On December 16, 2015, the Federal Reserve increased its benchmark interest rate by .25%. This was the first rate increase by the Fed in over nine years!

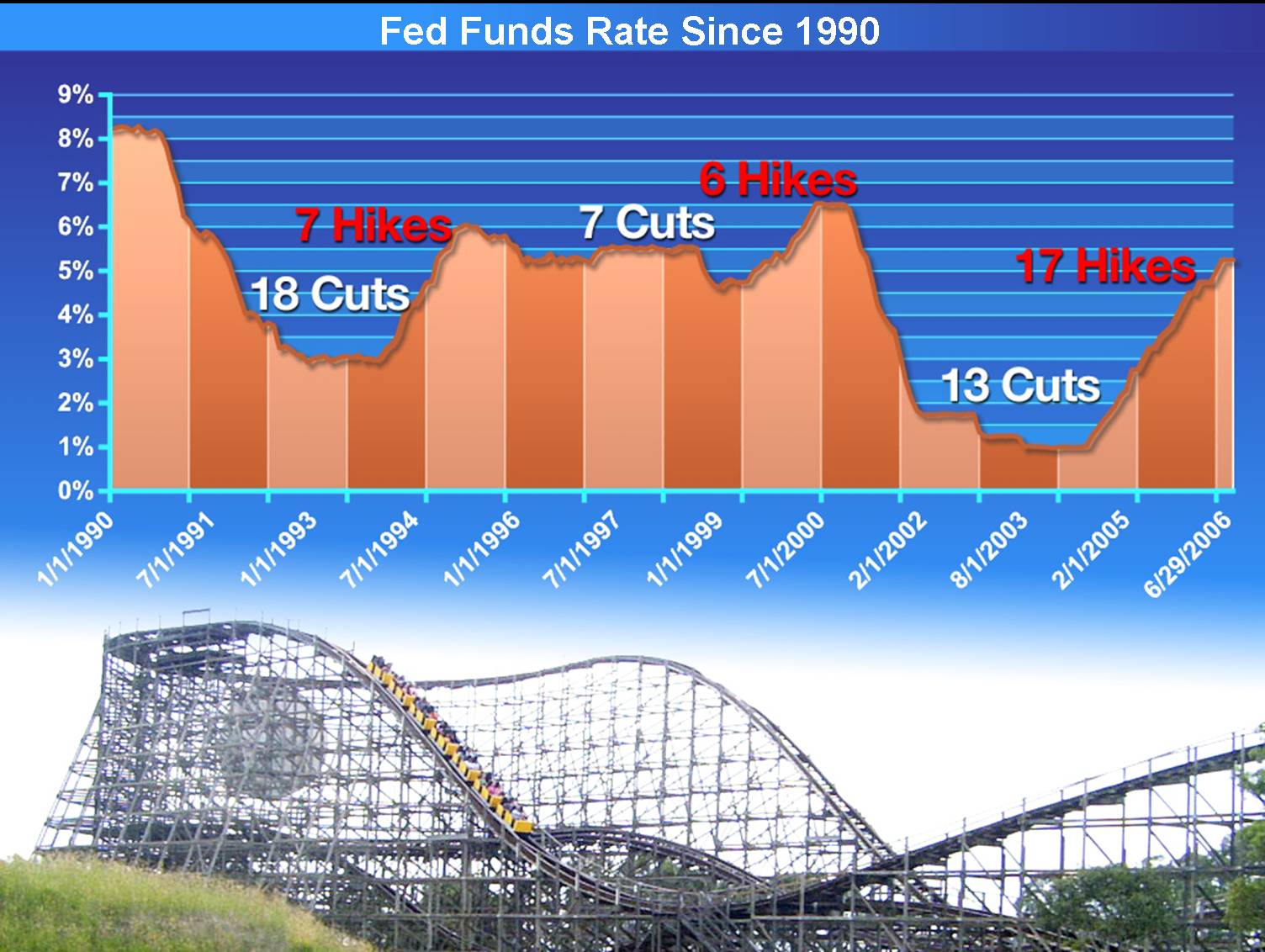

Generally the Fed makes interest rate moves in cycles. The chart shows the Fed Funds Rate rollercoaster over the past 25 years.

So what does this mean for you and your home loan?

Existing Loans

- Fixed Rate Mortgages – no affect. Loan terms on existing fixed-rate loans will not change.

- Adjustable Rate Mortgages (ARMs) – collateral affect. Generally the Fed changes also affects other rate indexes, meaning ARM loans may see increases during their adjustable period.

- Home Equity Lines of Credit (HELOCs) – direct affect. Most HELOC’s adjust based on the Prime Index, which is directly impacted by the Fed rate change. This means HELOCs may see increases during their adjustable period.

New Loans

Surprisingly, Fed rate increases don’t immediately increase mortgage rates. That’s because the Fed changes affect the Discount Rate and Fed Funds Rate, which is very different from mortgage rates. A mortgage rate can be in effect for 30-years, a rate that is set by the Fed can change day-to-day.

A closer look at historical moves by the Fed shows that its rate cuts often increase mortgage rates in the short term, while its rate hikes often decrease mortgage rates in the short term.

So ultimately, new home loans in the short term will NOT see immediate increases in rates due to the Fed rate hike.

However, the Fed’s move does give a general indication of the overall markets and economy, meaning the trend to come will be elevated interest rate levels.

Feel free to contact us if you have any questions regarding interest rates…we’re here to help!!